SISIP Financial,

Esquimalt Team

—

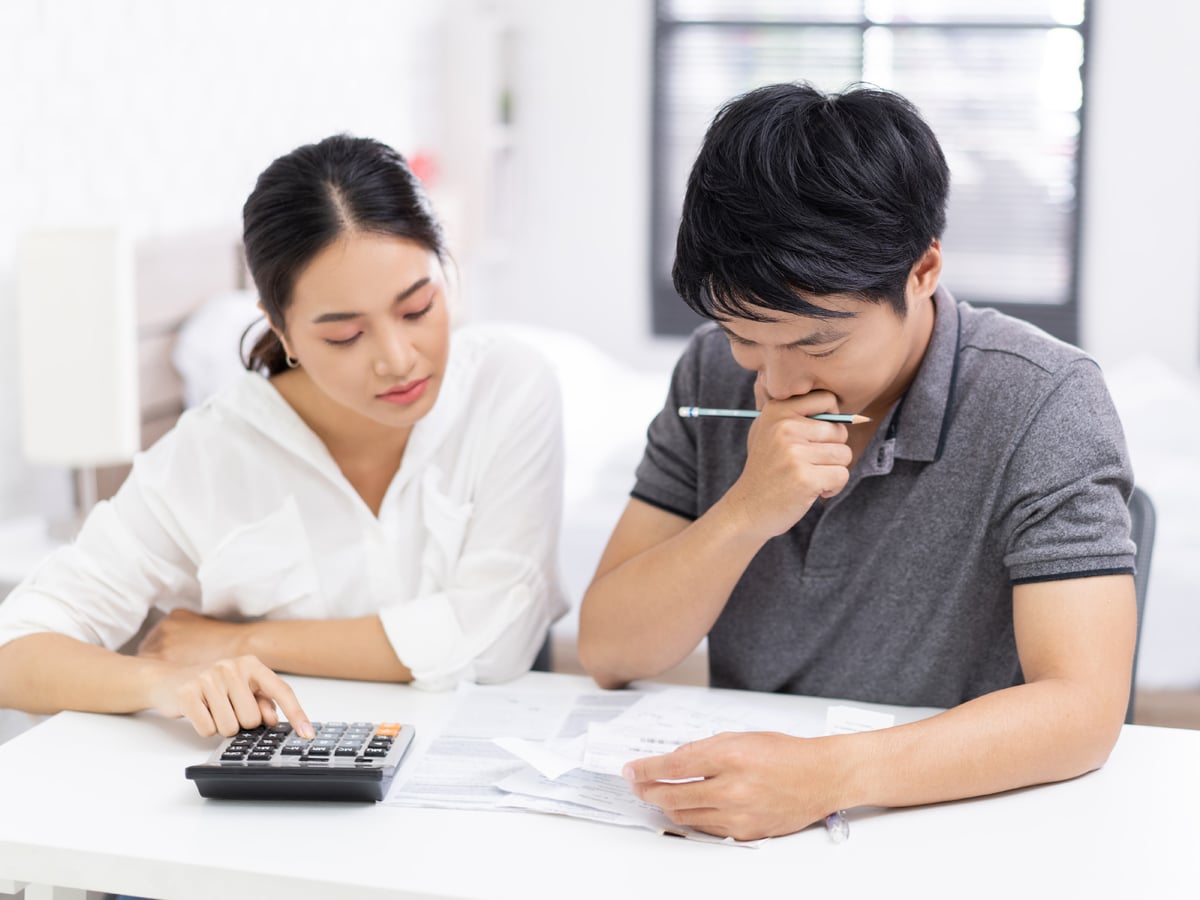

Military life often means sacrifices – frequent relocations, time apart, and sometimes, one spouse stepping back from a career to support the family. For many Canadian Armed Forces families, this can lead to uneven incomes and, eventually, uneven retirement savings. That’s where a spousal Registered Retirement Savings Plan (RRSP) can make a world of difference.

What is a Spousal RRSP?

A spousal RRSP is set up in one partner’s name but funded by contributions from the other partner. This arrangement is especially useful when one spouse earns significantly more than the other.

Here’s the key: The contributing spouse gets the immediate tax deduction, while the funds grow in the account of the lower-income spouse. When it’s time to withdraw the money in retirement, it’s taxed at the lower-income spouse’s rate, often saving the couple money on taxes overall.

Why Spousal RRSPs Work for Military Families

In military families, one spouse is often the primary breadwinner due to the demands of service. The other spouse may have a reduced or inconsistent income due to frequent relocations or childcare responsibilities. This income imbalance can create challenges in retirement, as the higher earner’s income from a CAF pension plus their RRSP could push them into a steep tax bracket.

A spousal RRSP helps balance this disparity by allowing the lower-income spouse to build retirement savings in their own name. Here’s why this matters:

- Lower Overall Tax Burden: Income splitting in retirement means less tax paid as a couple.

- Greater Financial Independence: The lower-income spouse has their own source of retirement income.

- Flexibility for Life’s Changes: If the lower-income spouse re-enters the workforce later, they can still decide to open an individual RRSP.

How Spousal RRSPs Work

- Contributions: The higher-income spouse contributes to the spousal RRSP.

- Tax Deduction: The contributor gets a tax deduction for the amount contributed, the same as they would with their own RRSP.

- Investment Growth: The investments grow tax-deferred, just like in a regular RRSP.

- Withdrawals: When funds are withdrawn in retirement, they’re taxed at the lower-income spouse’s rate.

Keep in mind that the contributions count against the higher-income spouse’s RRSP contribution room, and if funds are withdrawn within three calendar years of a contribution, the contributor may face taxes on the withdrawal.

It’s also good to know that contributions can continue until the recipient spouse turns 71. This means that, if the contributing spouse is older, they can keep saving taxes even when they are past the age limit.

Every family’s situation is unique. A SISIP advisor can help you understand how a spousal RRSP fits into your overall financial plan. Together, you can crunch the numbers, consider the options, and find the best strategy for your family.

Whether it’s reducing your tax bill now or setting up a smoother financial future, a spousal RRSP could be the missing piece of your retirement plan.

Contact our local SISIP office at 250-363-3301